Triple Crown Roofing: Prepare for Hurricane Season with Metal Roofing

What Your Roof Condition Means for Your Homeowners Policy

Florida homeowners are facing a new reality in 2026.

Insurance companies are tightening underwriting standards. Premiums are rising. Policies are being dropped. And one thing is under the microscope more than ever:

Your roof.

If your roof is over 10–15 years old — even if it’s not leaking — your homeowners' insurance could be affected.

At Triple Crown Roofing, we’re seeing this firsthand across Florida. Here’s what you need to know to protect your coverage, your home, and your investment.

Why Insurance Companies Are Focused on Roofs

Florida remains one of the highest-risk states for wind and storm damage. After years of hurricane claims, insurers are adjusting their requirements.

Here’s what’s happening:

- Roof age thresholds are being enforced more strictly

- 4-point inspections are required more frequently

- Wind mitigation reports are under closer review

- Policies are being denied or non-renewed based on roof condition alone

Even if your roof looks “fine,” insurers care about remaining useful life, not appearance.

The 10–15 Year Roof Rule (What It Really Means)

Most asphalt shingle roofs in Florida are rated for 20–30 years. But because of:

- Intense UV exposure

- High humidity

- Heavy rains

- Storm activity

Insurance carriers often consider a roof “high risk” once it reaches 10–15 years.

That doesn’t mean it must be replaced — but it does mean documentation becomes critical.

If you can’t show proof of condition or remaining life, your policy may be:

- Non-renewed

- Moved to a higher premium tier

- Required to replace the roof before renewal

What Is a 4-Point Inspection?

A 4-point inspection evaluates:

- Roof

- Electrical system

- Plumbing

- HVAC

When it comes to the roof portion, inspectors look for:

- Curling shingles

- Granule loss

- Soft decking

- Signs of leaks

- Previous patchwork repairs

If the inspector determines the roof has limited remaining life, the insurance carrier may require replacement — even if no active leak exists.

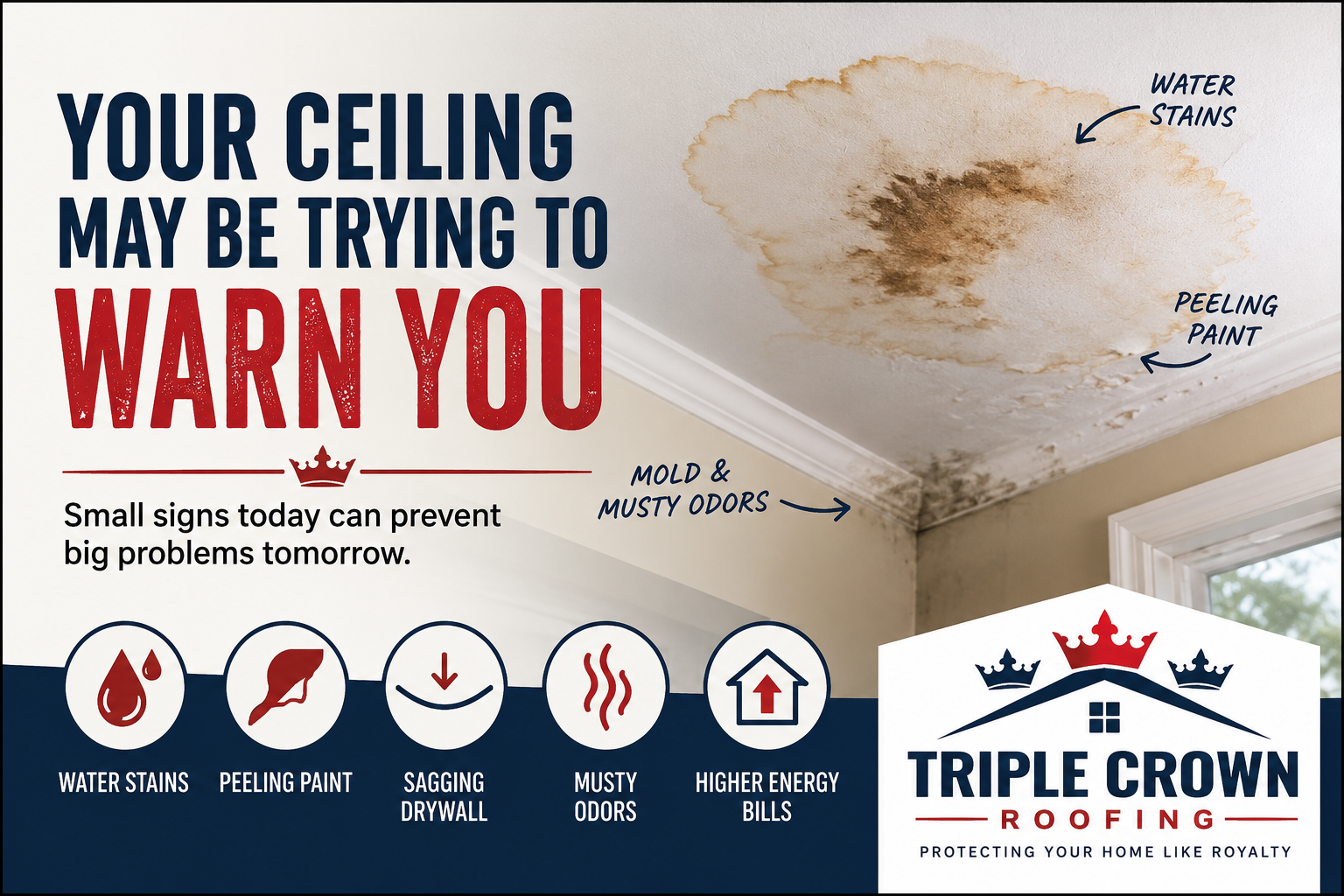

Signs Your Roof Could Affect Your Insurance

You don’t have to climb on your roof to notice warning signs. Look for:

- Shingles that are curling or lifting

- Granules collecting in gutters

- Dark streaking or algae growth

- Interior ceiling stains

- Loose flashing around vents or chimneys

If your roof is over 12 years old and showing any of these, it’s time for a professional inspection.

Repair vs. Replacement: What Insurance Cares About

Insurance companies are not evaluating based on cost savings — they are evaluating based on risk.

- Minor, isolated damage may qualify for repair documentation

- Widespread aging typically triggers replacement requirements

- Poor installation can shorten the acceptable lifespan

At Triple Crown Roofing, we provide detailed documentation and photo reports that homeowners can submit directly to their insurance carrier when needed.

Sometimes, the difference between policy renewal and cancellation is simply having proper documentation.

How to Prepare Before Your Renewal Date

If your policy renews within the next 6–12 months:

✔ Schedule a professional roof inspection

✔ Ask for documentation of remaining useful life

✔ Verify your wind mitigation credits

✔ Address minor repairs early

✔ Keep inspection records on file

Waiting until your insurer sends a warning letter limits your options.

Can a New Roof Lower Your Insurance Premium?

In many cases, yes.

Depending on materials and installation:

- Wind mitigation credits may apply

- Newer roofs reduce insurer risk profile

- Updated building code compliance may qualify for discounts

While every policy is different, many Florida homeowners see long-term insurance savings after replacing an aging roof.

The Bottom Line

Insurance companies aren’t targeting homeowners.

They’re managing risk.

And in Florida, your roof is one of the biggest risk factors on your property.

The good news?

You don’t have to guess.

Triple Crown Roofing helps homeowners understand their roof condition, prepare documentation, and make informed decisions before insurance companies are forced to act.

If your roof is 10+ years old — or if you have a renewal approaching — now is the time to act.

📞 Schedule a professional roof inspection

📋 Get documentation for your carrier

🛡 Protect your policy and your home

Your roof protects your home.

Make sure it protects your insurance coverage, too.

Don’t Wait fCancella